The life sciences sector is attracting more and more attention from real estate investors. This sector includes a wide range of industries, from

pharmaceuticals and biotechnology to medical devices and healthcare - all of which are expected to grow rapidly in the coming years, driven by advances

in medical technology and an ageing population. However, that does not mean that every life sciences location makes a worthwhile investment or is even

investable. It is incredibly important to be selective and attentive when seeking those life sciences locations (clusters, science parks and others) that have the potential to provide the most attractive risk-adjusted returns. The challenge is not easily met, because life sciences real estate in Europe has not yet matured as an asset class.

So, what drives success in a life sciences cluster? In this issue, we examine the term “cluster” and explain its nuances using European examples. We also identify the key drivers of cluster success. The current article is structured as follows: first, the term “cluster” is explained in generic terms. Then we group clusters into three broad categories, giving examples of each type. The article concludes by listing the five principal drivers of success and mentioning the types of data that can reveal the likelihood of an individual cluster’s future success.

UK examples of purpose-built science parks would be Oxford Science Park and Granta Park, Cambridge. Potsdam Science Park in Germany and Leiden Bio

Science Park in the Netherlands are examples from the continent. While not applicable to all, purpose-built parks tend to be held under single ownership. This allows curation of tenants and active asset management to drive real estate performance. There are many examples of parks developed

on greenfield or brownfield sites, which are typically low-rise in

landscaped environments with a range of on-site amenities and services.

Purpose-built science or innovation parks can also be found in urban settings. In these cases, where land supply tends to be limited, mid-size tower blocks allow scale and critical mass of tenants and can be designed in

a way to facilitate collaboration. With on-site amenities and access to the wider urban cultural infrastructure an attractive and productive ecosystem results. Two good examples are the recently developed White City Place in West London, located adjacent to the new Imperial College White City Campus, and Amsterdam Science Park located in the eastern part of Amsterdam. Trinity College Dublin has revealed ambitious plans for a €1 billion (£860 million) Grand Canal Innovation District (GCID), its proposed Innovation Hub near the

city centre.

2/ Clusters that develop and evolve

At an urban scale, London King’s Cross Knowledge Quarter (KQ) is a unique example of an urban cluster within a global city. KQ covers 260 ha (642 acres) around King’s Cross, Bloomsbury and Euston Road and describes itself as “home to the world’s greatest knowledge cluster”. It is anchored by the Francis Crick Institute, a partnership between six of the world’s leading

biomedical organisations – the Medical Research Council, Cancer

Research UK, the Wellcome Trust, University College London, Imperial College London, and King’s College London. The KQ captures a broad mix of science,

tech, art, history and culture, and the combined effect has been to create a vibrant and thriving ecosystem which is so critical in attracting and retaining talent. In addition to the number of academic institutions in the area, the regeneration around King’s Cross station and Pancras Square will host a number of high-profile global tech and media companies, such as Google, Facebook and Universal Music.

Covering a much broader urban geography, Genopole life sciences cluster, south of Paris, covers an area of 2,800 ha (6,919 acres) and provides 109,000 sq m (1.17 million sq ft) of accommodation for a diverse range of occupiers. Academic and medical links to the University of Paris-Saclay, University of Evry-Val-d’Essonne (UEVE) and the South Il-de-France Medical Centre (Centre Hospitalier Sud Francillien, or CHSF) generate talent and

start-ups. The cluster hosts over 100 member organisations and supports its own incubator and booster programmes with dedicated staff.

3/ Single-city or multi-city clusters

A third category is the city or cities cluster. Paris, Dublin and London

can be described as single city clusters. In each case, the cluster

is polycentric. For example, in London you find well-established locations such as King’s Cross and White City Place; however, in addition, London has a number of new science and innovation hubs in the development pipeline

that will add critical mass. Key locations include: Whitechapel (Royal London Hospital, NHS Property services), London Bridge Snowsfields Quarter (Guy’s and St. Thomas’, Foundation partnering with Oxford Properties and REEF), Royal Street (Guy’s and St Thomas’ Charity with Stanhope and The Baupost Group), Canary Wharf, where Canary Wharf Group and Kadans Science Partner are developing Europe’s largest commercial lab building over 22 floors.

Some industry commentators refer to the Oxford–Cambridge-London life sciences parks as the Golden Triangle as they are located across three UK

geographic regions. The Danish-Swedish life science cluster Medicon Valley describes itself as the crucible of Scandinavian life sciences. The bi-

national cluster spans the island of Zealand in Eastern Denmark and the Skåne-region of Southern Sweden.

The drivers of success

First, a caveat: success means different things to different people. For example, within the triple helix of academia, business and government, success could mean any of these:

The number of successful spinout companies or value of funds raised (universities)

Return on investment or ability to attract and retain talent (business)

Incremental economic growth or employment (government).

If we apply a quadruple helix (adding citizens) or a quintuple helix (adding the environment) framework, the list of definitions of success becomes

longer; however, these different interpretations of success can contribute to and overlap with each other.

It is important to have a clear understanding of the factors that contribute to the success of a cluster. In terms of the drivers of success, life science clusters have much in common with clusters in other parts of the knowledge economy such as the tech sector. In fact, the main drivers of success in the tech industry and across the knowledge economy in general

have been listed as: 1. A deep talent pool 2. Openness to people and ideas 3. The presence of local risk capital

A fourth factor to consider is, whether the cluster has the support of government (both local and national) and business leaders. In life sciences, this is critical (although it seems that government support has been a mixed blessing in the tech sector). There is one other driver, although it may be less significant as a cluster matures, and it is the availability of alternative work if a start-up fails. The presence of established life sciences players can be helpful here, but not decisive because clusters have to start from somewhere. Clusters, science parks and innovation districts that score highly on at least four of these five drivers are well positioned to succeed in the life sciences sector in the years ahead.

Quantifying the drivers of success

We have identified the key drivers, but the real challenge is measuring

the strength of each driver in any given location. For example, there is no single benchmark that encapsulates the depth of the talent pool in a city or county; however, it is possible to assemble a composite measure drawn from

various sources. (The quality of research is one indicator here and cities with strong science- based universities like Berlin,Cambridge, Dublin, London, Munich, Oxford, Paris, Utrecht and Zurich should score well under this heading).

The same applies to the second driver of success, openness to people and ideas – a single benchmark does not exist, but a composite measure comprising many indicators may be possible instead. (Tolerance of minorities is one indicator here).

The third driver of success, the presence of local risk capital, can be assessed by tracking historic deal flow. Funding is the lifeblood of new and growing life sciences businesses and the sums of venture capital (VC) being

raised in the biotech sector has reached record levels. Globally, €33.9 billion (£28.1 billion) was raised in 2021, an increase of 10 per cent over 2020. Successful capital raising brings forward spinouts, start-ups, scale-ups and driving expansion. This in turn drives strong occupier demand requirements for a range of appropriate real estate in specific locations where the talent pool and ecosystem overlap.

The fourth and fifth factors, government support and the availability of alternative work, are generally quantifiable using publicly available statistics.

The benefits of clustering

The effects that these clusters have on innovation and productivity growth are quite impressive, even on the individual level. According to American research, “in biology and chemistry, a move from the median cluster (Boise, Idaho) to the 75th percentile cluster (State College, Pennsylvania) is associated with a productivity gain of 8.4 per cent, holding constant the inventor and the firm.”

Science parks and larger clusters have the same ultimate goal

While having similar occupiers and objectives to a science park, science-based clusters, with a multiple-ownership structure, will tend to grow organically at scale, rather than in a more curated fashion associated with single- ownership purpose-built science parks. They will likely cover a

broad geography, sometimes crossing international borders and will contain a comprehensive mix of office, R&D, lab and manufacturing premises. Clusters,

through their larger geographical spread, will have access to several universities, higher education establishments, and university teaching hospitals.

However, the goals are the same – academic and business collaboration, nurturing the growth of spinouts, start-ups and SMEs, cross-pollination of

ideas and research, innovation of new product, and acceleration to market. The importance of strong digital infrastructure and international connectivity should not be underestimated in the success of large clusters.

Three types of clusters

It could be argued that clusters are one of three types. First, there are purpose-built science parks located within proximity of academic and medical facilities. Second, there are clusters that develop and evolve around

academic or medical centres of excellence utilising a mix of new, existing, and repurposed buildings and redevelopment of obsolete commercial space. Third, there are what might be termed “city or cities clusters” where several science parks or other “areas of innovation” form part of a citywide

or even regional cluster network.

The drivers of cluster success

It is important to have a clear understanding of the factors that contribute to the success of a cluster. In terms of the drivers of success, life science clusters have much in common with clusters in other parts of the knowledge economy such as the tech sector. In fact, the main drivers of success in the tech industry and across the knowledge economy in general

have been listed as: a deep talent pool; openness to people and ideas;

and the presence of local risk capital. Clusters, science parks and

innovation districts that score highly on these drivers are well positioned to succeed in the life sciences sector in the years ahead.

We have identified the key drivers, but the real challenge is measuring the strength of each driver in. The main drivers of success are a deep talent pool, openness to people and ideas, and the presence of local risk capital. For example, there is no single benchmark that encapsulates the depth of the

talent pool in a city or country; nevertheless, it is possible to assemble a composite measure drawn from various sources.

The quality of research is one indicator of talent, and cities with strong science-based universities like Berlin, Cambridge, Copenhagen, Dublin, London, Munich, Oxford, Paris, and Zurich score well under this heading.

Having a high number of life sciences firms already established in a location is another indication of a deep talent pool.

The second driver of success, openness to people and ideas, also lacks a single benchmark. However, a composite measure comprising several indicators may be possible instead. Tolerance of minorities is one important indicator, because as The Economist notes: “Migrants are a disproportionately enterprising bunch. Around 60 per cent of America’s most valuable tech

companies were started by immigrants or their children. European hubs such as Berlin, London and Paris, each of which is home to ten or more unicorns, have large immigrant populations.” The ability to attract talented people from abroad, sometimes called “brain gain”, is another important indicator.

The third driver of success, the presence of local risk capital, can be assessed by tracking historic deal flow and by examining the local investors. How many life sciences companies have raised more than $10m? Are the local investors “seasoned” (that is, have they seen prior investments

through to exit)? Successful capital raising brings forward spinouts, start-ups, scale-ups and driving expansion. This in turn drives strong occupier

demand requirements for a range of appropriate real estate in specific locations where the talent pool and ecosystem overlap.

The data

Using data from the World Economic Forum, Gallup (the American analytics and

advisory company), the Leiden Ranking (which charts the academic performance of 500 major universities throughout the world), Crunchbase, and elsewhere allows us to gauge the performance of a cluster using a framework built around the three key drivers of success.

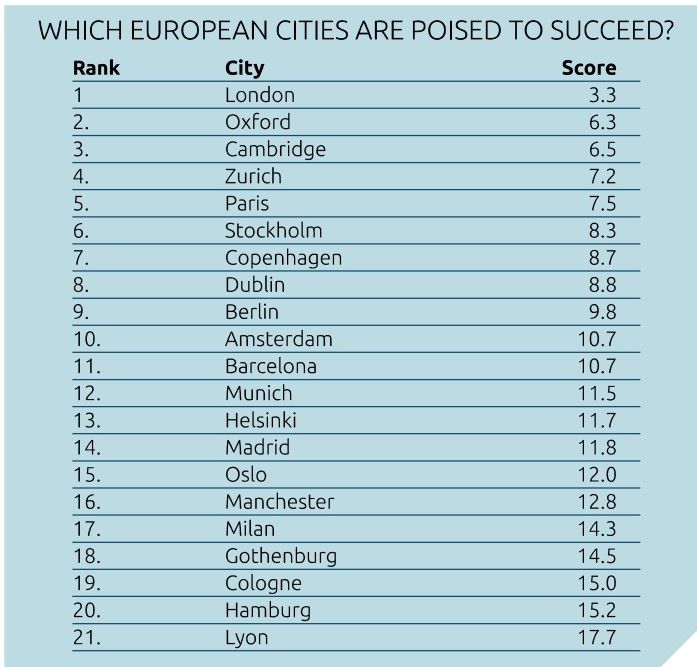

To illustrate this framework, we apply it to the group of 21 European cities that feature in the report “European Start-up Hotspots: An Analysis based on

VC-backed Companies”, published by the European Union. That report provides evidence on start-up activity in Europe and describes European VC activity

over the previous two decades. The study notes that 28 per cent of all

European VC-backed companies are based in this group of 21 cities, which is led by Paris, London and Berlin. The framework could, of course, be extended to include other cities. The table shows the results.

The drivers of success are equally weighted in this example but, of course, one could flex the weightings (for example, by focusing more on openness to

people and ideas and less on the presence of local risk capital). The

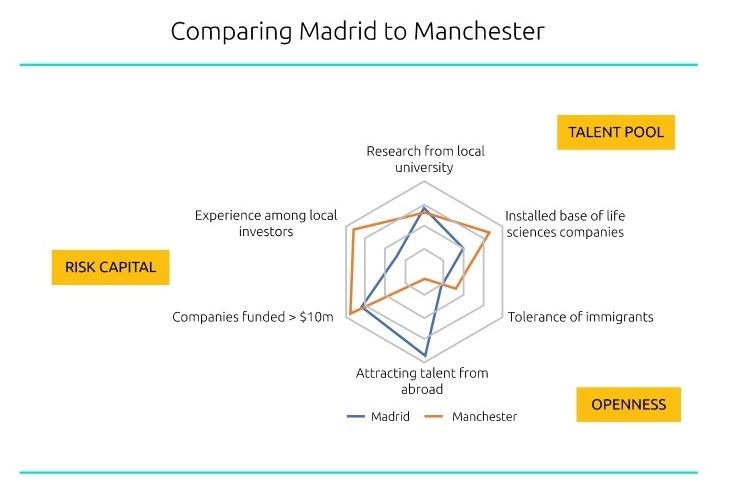

spiderweb chart below illustrates how Madrid and Manchester ended up with very similar overall scores even though the two cities have different strengths and weaknesses. (In the chart, a score near the centre is better

than a score near the perimeter.) Manchester is better at attracting talent from abroad, which is an indicator of openness to people and ideas, but Madrid has more experienced local investors and ‘therefore’ scores better on risk capital.

Conclusion

Successful clusters in the life sciences sector and the wider knowledge economy are driven primarily by a deep talent pool, openness to people and ideas, and the presence of local risk capital. There are secondary

drivers too, but these three dominate. There is no single and authoritative benchmark for the primary drivers, but we have demonstrated that the strength of the three drivers can be estimated by weaving together data from diverse sources.